The power of a Private Limited Company with the freedom of a Sole Proprietorship. Start your corporate journey with a separate legal identity and limited liability today.

Application Form for

One Person Company Registration in Kottayam

Fill in the details to get registered

INTRODUCTION

What is a One Person Company?

A One Person Company (OPC) is a business structure introduced under the Companies Act, 2013 for solo entrepreneurs. It allows a single individual to own and operate a corporate entity with limited liability protection, a separate legal identity, and continuity beyond the owner’s lifetime.

OPCs combine the benefits of a sole proprietor’s simplicity with the credibility and protection of a company — ideal for freelancers, small business owners, and early-stage founders who want a low-compliance corporate vehicle.

Single owner, full control

Owner acts as director & shareholder.

Limited liability

Personal assets protected from business debts.

Corporate status & credibility

Easier to get loans, contracts and partners’ trust.

Minimal compliance

Simpler reporting vs a Pvt Ltd; no AGM requirement.

Why register an OPC?

Registering an OPC gives legal recognition, protects personal assets, ensures continuity through a nominee, and improves credibility for loans and clients — all with comparatively relaxed compliance.

Note: OPCs must convert to a Private Limited Company once they exceed ₹2 crore turnover or ₹50 lakh paid-up capital.

Advantages of OPC

Why solo founders prefer OPC over Proprietorship

Limited Liability

The biggest advantage. Your liability is restricted to the unpaid share capital. Your personal savings/assets are safe.

Legal Status

OPC is a separate legal entity. It can own property, sue, and be sued in its own name, unlike a proprietorship.

Banking & Loans

Banks and financial institutions prefer lending to companies (OPCs) rather than proprietary firms.

Perpetual Succession

With a clearer nominee structure, the business continues to exist even in the event of death or disability of the owner.

Less Compliance

OPCs have exemptions from holding AGMs and other procedural compliances required for Private Limited companies.

Brand Protection

Your company name is protected. No one else can start a company with the same name in India.

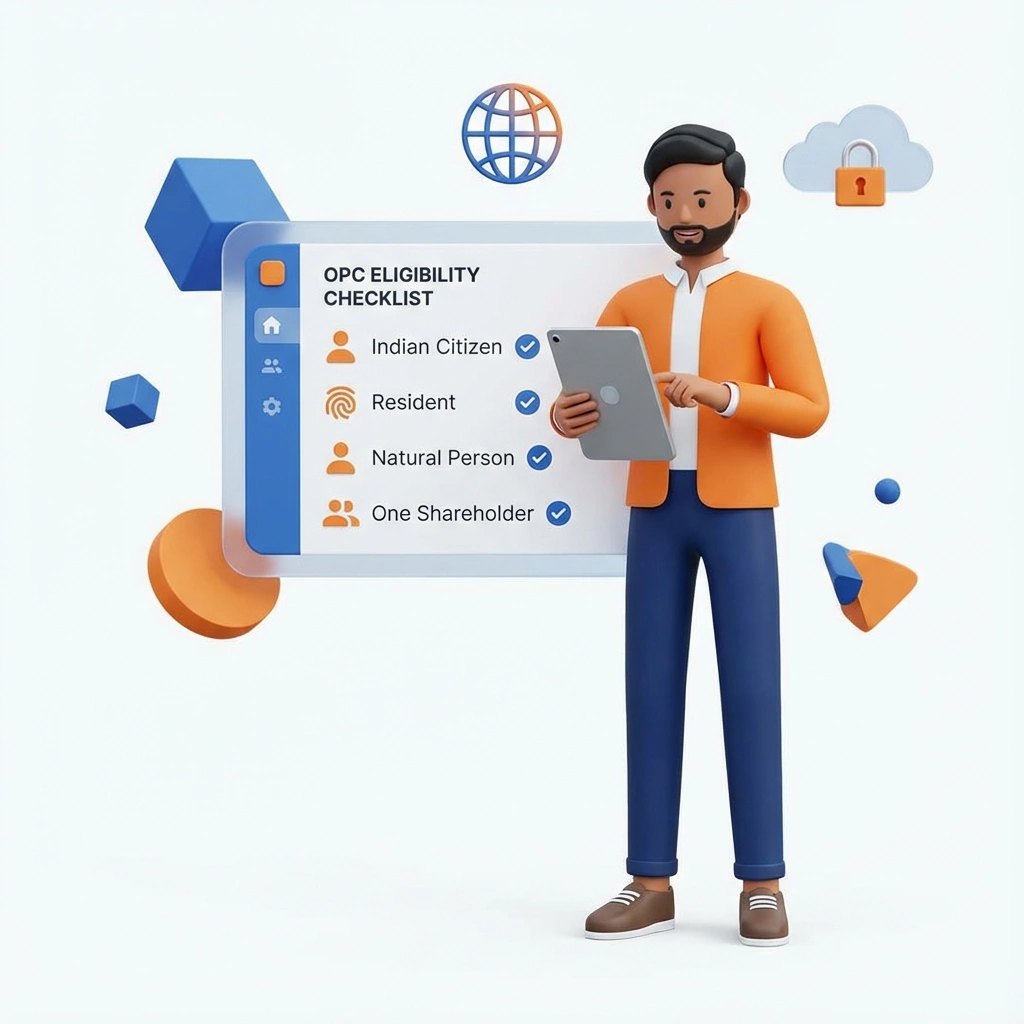

Eligibility Criteria

Who can form an OPC?

Valid for Indian Citizens and Residents only.

Only 1 Person can be the member/shareholder.

Must appoint a Nominee (must also be an Indian Resident).

Cannot be a minor.

Conditions & Restrictions for OPC Registration

While an OPC offers flexibility and strong legal protection, the Ministry of Corporate Affairs (MCA) imposes certain conditions you must be aware of:

•

Only One OPC Per Person: An individual can incorporate or be a nominee in only one OPC at a time.

•

No Public Fundraising: OPCs cannot issue shares to the public or be listed on the stock exchange.

•

Mandatory Conversion: Once the company exceeds ₹2 crore turnover or ₹50 lakh paid-up capital, it must convert to a Private Limited Company within 6 months.

Address Proof: Bank Statement / Mobile Bill (Latest)

Passport size photographs

Office Address Proof

Electricity Bill (Not older than 2 months)

Rental Agreement (if rented)

NOC (No Objection Certificate) from landlord

STEP BY STEP

OPC Registration Process

Follow these steps to successfully register a One Person Company (OPC) in India as per MCA guidelines.

1

Obtain a Digital Signature Certificate (DSC)

Necessary for online authentication and secure submission of documents.

2

Apply for Director Identification Number (DIN)

Unique ID assigned to the director for regulatory compliance.

3

Reserve Company Name via RUN Form

Secure a distinct company name through the Ministry of Corporate Affairs (MCA).

4

Prepare Memorandum & Articles of Association (MoA & AoA)

Define business objectives, governance, and operational structure.

5

Submit SPICe+ Form

A unified application for OPC incorporation, streamlining the registration process.

6

Pay Government Fees & Stamp Duty

Charges vary by state and must be paid for successful registration.

7

ROC Verification & Approval

The Registrar of Companies (ROC) examines the application and documents.

8

Receive Certificate of Incorporation

Official document confirming the OPC’s legal establishment.

9

Apply for PAN & TAN

Essential tax registration numbers for financial and business compliance.

✓

Set Up a Business Bank Account

Enables financial transactions and ensures smooth operations — final step to get your OPC up and running.

Post-Registration Compliance for OPC

After incorporation, an OPC must follow certain statutory filings and compliance steps to remain in good standing. Below are the key obligations to note.

1

Annual Filings & Financial Reporting

File AOC-4 (financial statements) and MGT-7A (annual return) with the ROC annually. Financial records must be audited; non-compliance attracts penalties.

2

Taxation & GST Compliance

OPCs are taxed as companies. Ensure timely income-tax filings. Register for GST if turnover crosses thresholds and file regular GST returns (GSTR-1 / GSTR-3B / annual reconciliations) to avoid penalties.

3

Conversion Triggers

An OPC must convert to a Private Limited Company when paid-up capital exceeds ₹50 lakh or annual turnover exceeds ₹2 crore (trigger rules apply). Monitor thresholds and act within prescribed timelines.

4

Accounting & Audit

Maintain proper books of account and get annual audits done by a qualified auditor (where applicable). Retain supporting records for statutory inspection and tax assessments.

5

Statutory Registers & ROC Filings

Keep statutory registers updated (partners, charges, minutes). File necessary ROC forms (changes in director/nominee, registered office, etc.) within the prescribed timelines.

6

Other Compliance & Misc.

Maintain compliance for payroll (TDS), PF/ESI (if applicable), workplace safety, and timely statutory notices. Appoint nominee and update records for smooth succession.

Tip: Keep a compliance calendar (due dates for ROC, tax & GST) and consult your CA to avoid penalties and conversion surprises.

Frequently Asked Questions

An OPC is a business structure where a single individual owns and operates a company with limited liability, offering the benefits of a corporate entity.

Any Indian citizen and resident (living in India for at least 182 days in the previous financial year) can register an OPC.

Yes, an OPC can have more than one director, but it can only have one shareholder or owner who controls the company.

No, an OPC can be registered with any amount of capital, as there is no legally mandated minimum capital requirement.

Yes, appointing a nominee is mandatory to ensure business continuity if the sole owner becomes incapacitated or passes away.

Yes, voluntary conversion is allowed anytime, and mandatory conversion is required if turnover exceeds ₹2 crore or paid-up capital surpasses ₹50 lakh.

Yes, OPCs cannot engage in financial activities like banking, insurance, or investment in other companies’ securities.

OPCs must file annual financial statements, income tax returns, and required compliance documents with the Registrar of Companies (ROC).

Yes, an OPC can voluntarily convert into a Private Limited Company by fulfilling legal procedures and compliance requirements.

No, OPCs are exempt from holding an AGM, and financial statements are directly approved by the sole member.

No, OPCs cannot register as a Section 8 company, which is required for non-profit or charitable activities.

No, only an individual Indian resident can be the sole member and nominee of an OPC.

If the owner becomes a non-resident, the OPC must convert into a Private or Public Limited Company within six months.

No, an individual cannot register or be a nominee in more than one OPC at a time.

No specific tax benefits exist for OPCs. They are taxed at 25% as per corporate tax laws applicable to private limited companies.

LOCATIONS

One Person Company Registration in Kottayam in Different States